DariaRen

By Tajinder Dhillon

The peak duration of incomes season begins today and we sneak peek the S&P 500 2023 Q4 incomes season in granular information, supplying both aggregate and company-level insights utilizing information from I/B/E/ S, StarMine, and Datastream, which are all discovered in the desktop service LSEG Work area.

Revenues Commentary

2023 has actually been far much better than anticipated, as every quarter (Q1, Q2, and Q3) saw an enhancement in the last incomes development rate compared to the start of incomes season while directly preventing an ‘incomes economic downturn.’

Throughout the very first 3 quarters of 2023, Q4 incomes development expectations stayed steady. Nevertheless, over the last 3 months, experts have actually strongly reduced expectations by 640 basis points, much more than what we generally see heading into incomes season.

The only intense area was Infotech, the only sector to see both its incomes development and net earnings margin expectations increase, heading into incomes season. The Splendid 7 have an aggregate incomes development rate of 52.2% this quarter and are when again pressing the index into favorable incomes area. If the Mag 7 is omitted, incomes development decreases to -3.2%.

More worrying is the trajectory of incomes momentum keeping an eye out into 2024, as 7 sectors have actually seen down modifications to incomes development for Q1, Q2, and Q3. Full-year development expectations for 2024 have actually decreased by 100 basis points over the last 3 months to 11.1%, however are still above the long-lasting average of 7.6%.

Part 1 – Revenues Development and Contribution

Utilizing information from the January 19th publication of the S&P 500 Revenues Scorecard, Q4 mixed incomes (integrating quotes and actuals) are anticipated at $454.2 billion (+4.5% y/y, -7.3% q/q) while income is anticipated at $3,867.7 billion (+2.5% y/y, +1.4% q/q).

Ex-energy, incomes development is anticipated at 8.2%, which marks the 3rd successive quarter of favorable ex-energy development. Ex-energy, income development is anticipated at 3.8%.

At a sector level, Industrials is presently anticipated to snap its streak of favorable y/y incomes development at eleven successive quarters, the longest of any sector. Customer Discretionary, Customer Staples, and Financials are all anticipated to see a 4th successive quarter of development. Products is anticipated to publish a 6th successive quarter of incomes decrease followed by Healthcare for 5 successive quarters.

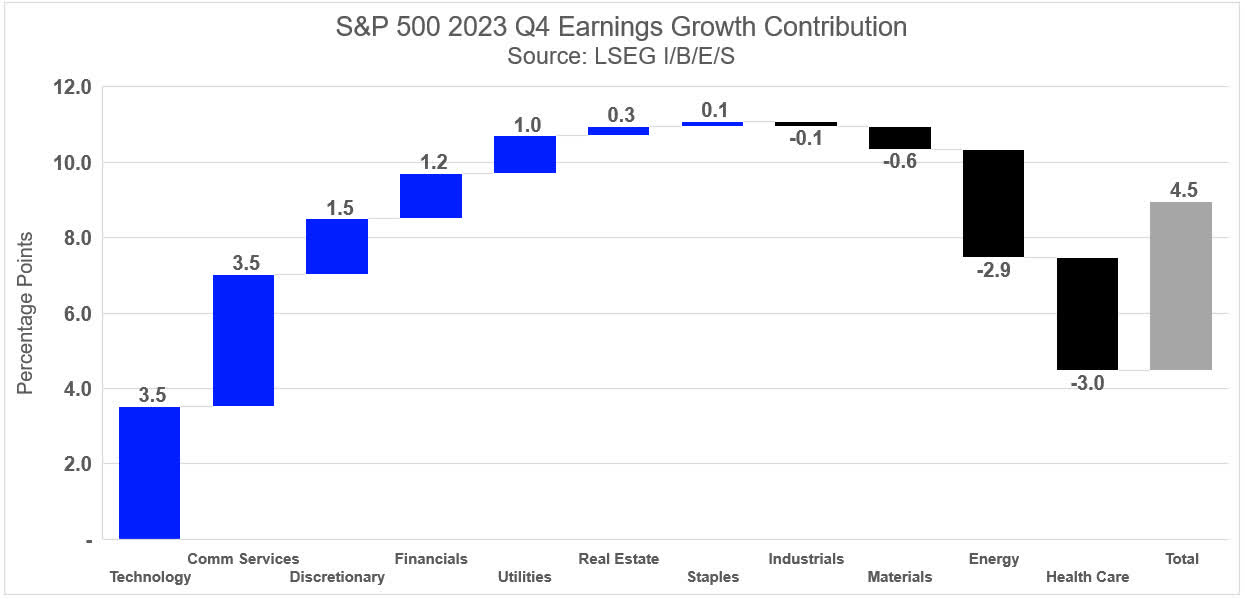

From an incomes development contribution point of view, 7 sectors have favorable incomes contributions while 4 sectors have unfavorable incomes contributions (Exhibition 1).

Interaction Solutions has the biggest development contribution of any sector and is anticipated to contribute 3.5 portion points (PPT) towards the index development rate of 4.5%. Infotech (3.5 ppt) and Customer Discretionary (1.5 ppt) are the next biggest factors while Healthcare (-3.0 ppt), Energy (-2.9 ppt), and Products (-0.6 ppt) are the biggest critics to incomes development this quarter.

Exhibition 1: S&P 500 Q4 2023 Revenues Development Contribution

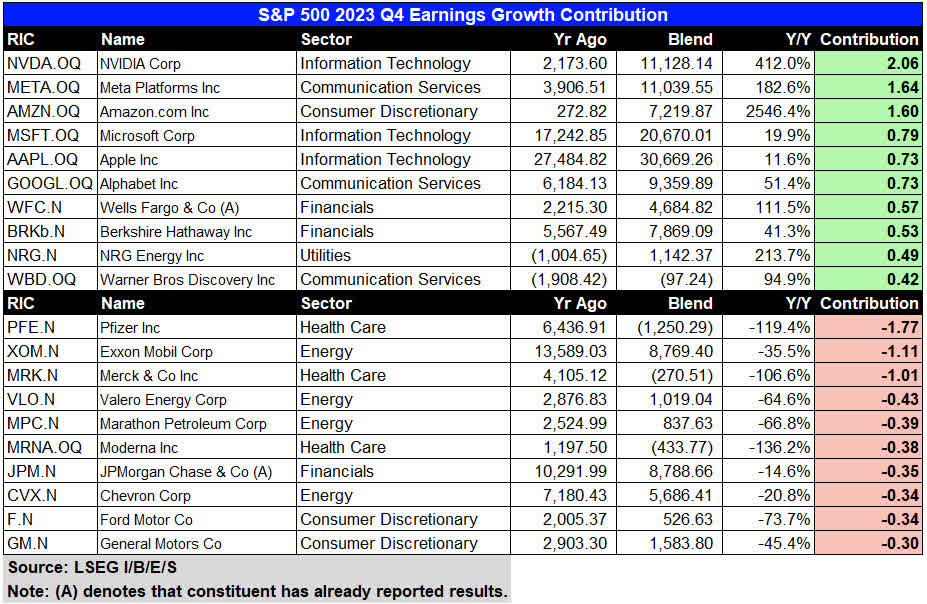

We likewise take a look at incomes development contribution at a constituent level in Exhibition 1.1 and highlight the leading 10 and bottom 10 factors. Nvidia ( NVDA), Microsoft ( MSFT), and Apple ( AAPL) are anticipated to provide the lion’s share of incomes development for Infotech. The exact same can be stated for Amazon ( AMZN) in Customer Discretionary for the 4th successive quarter (1.6 ppt), and Meta ( META) and Alphabet ( GOOG) ( GOOGL) for Interaction Solutions. To put it simply, the “Splendid 7” will yet once again be a group to take a look at carefully this quarter.

In the bottom half of the table, Energy controls the leading 10, provided hard year-over-year contrasts. For the 4th successive quarter, a number of the big pharmaceutical constituents are anticipated to publish unfavorable incomes development from a strong 2022 when they gained from vaccine incomes.

Exhibition 1.1: S&P 500 Q4 2023 Revenues Development Contribution

Part 2 – Price Quote Revisions into Revenues Season

Experts have actually strongly reduced incomes expectations heading into incomes season to levels we have not seen considering that 2022. From an assistance point of view, we have actually seen 75 unfavorable Q4 EPS pre-announcements compared to 37 positives, leading to a negative/positive ratio (n/p) of 2.0, which is listed below the long-lasting average of 2.5 and in line with the previous four-quarter average of 2.1. In Q3, we saw 79 unfavorable pre-announcements compared to 41 favorable heading into incomes season, yielding a 1.9 n/p ratio.

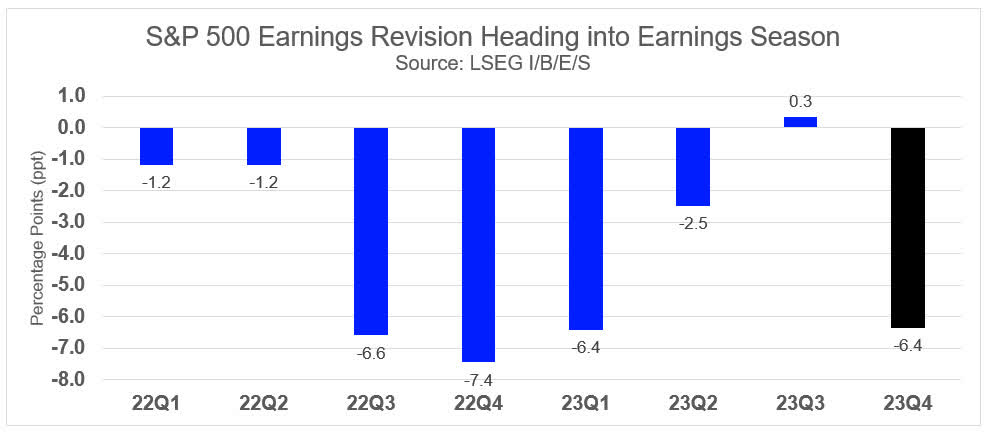

Over the last 3 months, the Q4 EPS price quote has actually decreased from $58.14 to $54.27 per share, leading to experts reducing y/y development expectations by 6.4 ppt heading into incomes season (Exhibition 2). Q4 development expectations peaked in the week ending September 29 (+11.0%) and have actually considering that fallen 13 out of the last 15 weeks.

Exhibition 2: S&P 500 Revenues Modifications

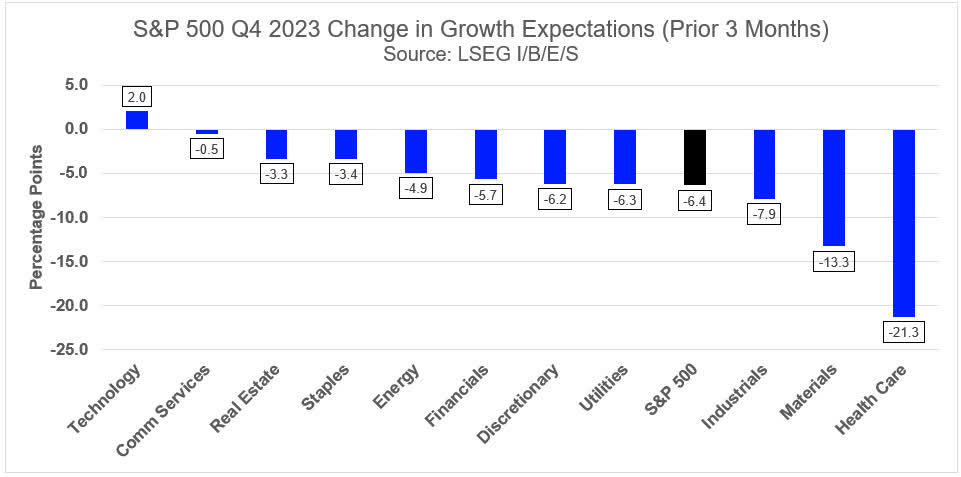

Exhibition 3 highlights incomes momentum at a sector level, specified as the rate of modification in Q4 development expectations over the last 3 months, revealed in portion points. All however one sector has actually seen a favorable incomes momentum this quarter as Infotech has actually seen quotes increase by 2 portion points. Products has actually seen the weakest momentum for the 2nd successive quarter (-13.3 ppt) followed by Industrials (-7.9 ppt), and Energies (-6.3 ppt).

Over this exact same duration, Infotech has actually seen an upgrade in incomes development expectations for the next 3 quarters (consisting of Q4). On The Other Hand, Customer Staples has actually seen a downgrade in incomes development expectations for the next 5 quarters (consisting of Q4). Customer Discretionary, Energy, Industrials, Products, Property, and Interaction Solutions have actually all seen a downgrade in incomes development expectations for the next 4 quarters (consisting of Q4).

Exhibition 3: S&P 500 2023 Q4 Price Quote Modifications

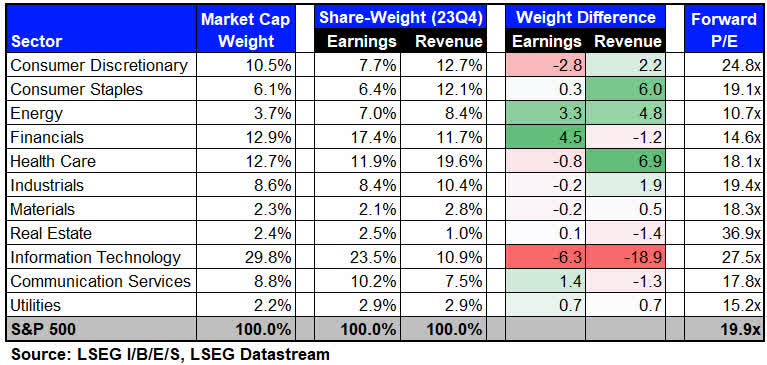

Part 3 – Market Cap vs. Revenues Weights

Exhibition 4 takes a look at the distinction in between ‘market-cap’ and ‘share-weighted’ weights for the S&P 500 sectors. The S&P 500 Revenues Scorecard makes use of a share-weighted method.

Infotech has the biggest incomes weight this quarter at 23.5% which has to do with 6 portion points lower than its market-cap weight of 29.8%. This leads to the biggest unfavorable weight differential of all sectors, highlighting the premium on the sector, which has a forward P/E of 27.5 x (38% premium vs. S&P 500).

Financials saw an increase to its incomes weight in Q1 due to the GICS Category modification in March, which saw juggernauts Visa ( V) and Mastercard ( MA) relocate to this sector (formerly living in Infotech). To learn more about this, please take a look at our previous note on this topic: 2023 GICS Category Modification: Effect On S&P 500 Revenues, March 27, 2023 The sector has the biggest favorable incomes weight differential at 4.5% with a forward P/E of 14.6 x.

While Energy’s favorable weight differential has actually decreased compared to previous quarters, the sector continues to overdeliver on incomes relative to its market cap weight (which has actually doubled considering that September 2021) and trades at the most affordable assessment of any sector at 10.7 x.

The Splendid 7 group – Apple, Amazon, Alphabet, Meta, Microsoft, NVIDIA, and Tesla ( TSLA) has a market cap weight of 28.8% (simply listed below an all-time high) compared to an incomes and income weight of 20.3% and 11.2% respectively. The Splendid 7 group has an aggregate forward four-quarter P/E of 29.1 x, a 46% premium to the total index. When leaving out the Mag 7, the forward P/E decreases to 17.5 x.

Exhibition 4: Market Cap vs. Share-Weight for S&P 500 Sectors

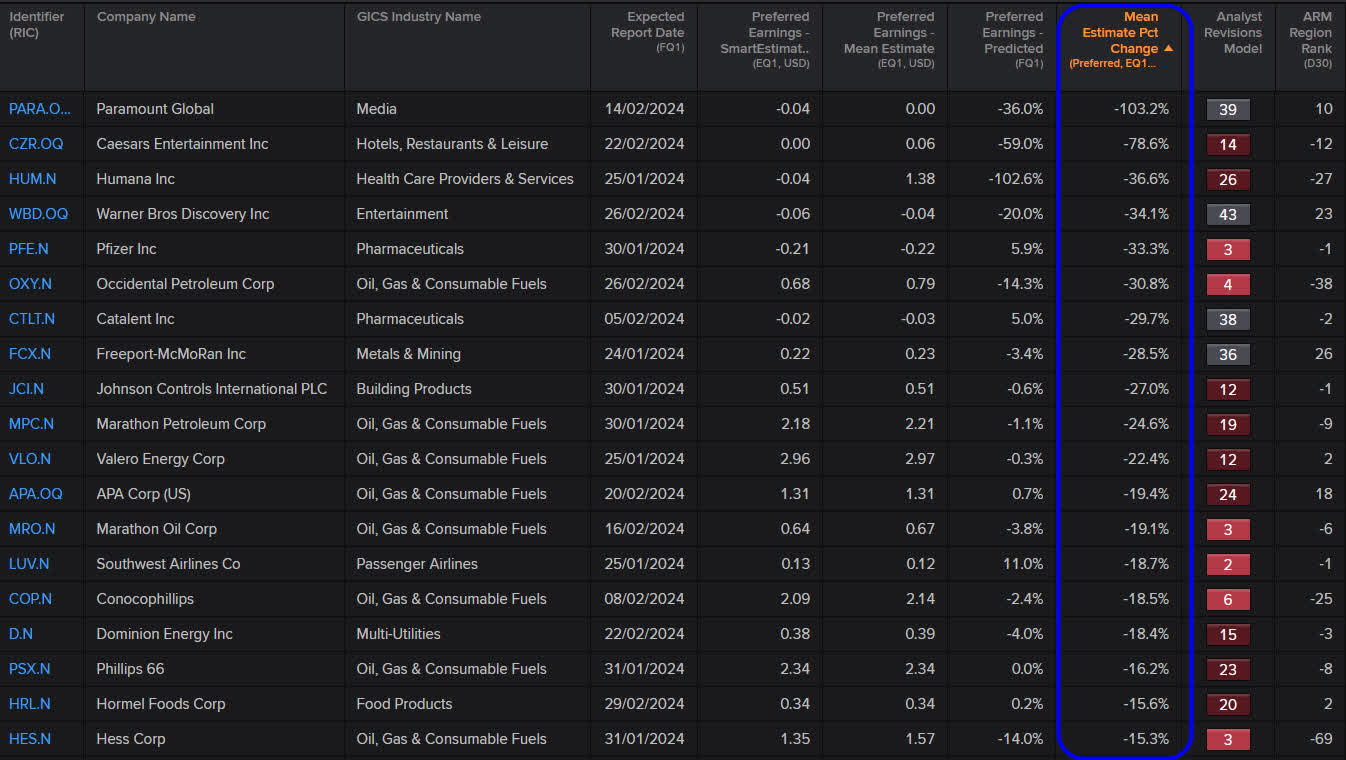

Part 4 – Which business have seen the biggest modifications heading into incomes season?

Utilizing the Screener app in LSEG Work area, we can evaluate for yet-to-report constituents that have actually seen the biggest upgrades and downgrades heading into incomes season.

Exhibition 5 highlights business who have actually seen incomes downgrades as specified by the 60-day mean price quote modification in ‘EQ1 Preferred Revenues’. Preferred Revenues is specified as EPS for many business other than for Property where it can be either EPS or FFOPS depending upon expert protection.

Paramount Global ( PARA) has actually seen the biggest downgrade in EPS approximates over the last 60 days (-103.2%) followed by Caesars Home entertainment, Inc. ( CZR) (-78.6%), Humana ( HUM) (-36.6%), Warner Bros Discovery, Inc. ( WBD) (-34.1%), and Pfizer Inc. ( PFE) (-33.3%). Note: worths less than -100% happen when an EPS price quote turns from favorable to unfavorable.

Exhibition 5: Largest Unfavorable Modifications for 2023 Q4

LSEG Office

Exhibition 5 likewise shows the StarMine Predicted Surprise (PS%) for each constituent, which compares the SmartEstimate vs. Mean Quote. The PS% is an effective quantitative analytic that compares the StarMine SmartEstimate to the agreement mean. The SmartEstimate positions a greater weight on experts who are more precise and timelier, hence supplying a refined view into agreement. Comparing the SmartEstimate © to the mean price quote results in our PS%, which properly forecasts the instructions of incomes surprise 70% of the time when the PS% is higher than 2% or less than -2%.

The StarMine SmartEstimate is a quantitative analytic that is utilized as an input to a number of the StarMine designs.

We see a favorable connection in between constituents who have actually seen a big downgrade and a matching unfavorable PS. Moreover, a favorable connection is revealed in between the mean price quote modification vs. Expert Modification Design (ARM) rating (i.e., business that have actually seen big down incomes modification likewise have a low ARM rating).

ARM is a percentile stock ranking design that is created to forecast future modifications in expert belief by taking a look at modifications in quotes throughout EPS, EBITDA, Earnings, and Suggestions over numerous period. The last 2 columns show both the present ARM rating and its 30-day modification.

Taking A Look At the Predicted Surprise and ARM columns can be really helpful throughout incomes season to evaluate the probability of whether business are anticipated to beat or miss out on incomes while at the exact same time evaluating expert belief.

The screener app supplies an effective workflow tool for Experts and Portfolio Supervisors aiming to parse through numerous business throughout incomes season to determine thematic patterns.

Exhibition 5.1 shows the exact same information for constituents with the biggest upgrades heading into incomes season.

Exhibition 5.1: Largest Favorable Modifications for 2023 Q4

LSEG Office

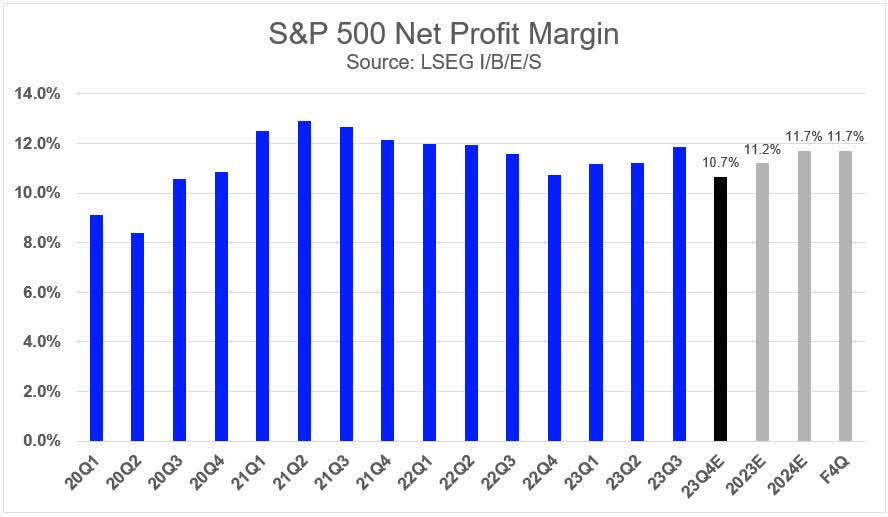

Part 5 – Net Earnings Margin Expectations

Utilizing information from the S&P 500 Revenues Scorecard, we take a look at quarterly net earnings margins (Exhibition 6). Net earnings margins peaked in 2021 Q2 (12.9%) which then decreased for 6 successive quarters and has actually considering that increased for 3 successive quarters.

The Q4 mixed net earnings margin is 10.7%, a 50-basis point decrease from the previous quarter, and will possibly end a three-quarter successive enhancement in margins. We keep in mind that Q4 margin expectations have actually slowly decreased over the last 3 months.

Over the last 3 months, 10 sectors have actually seen net margin price quote decrease, while one sector has actually seen a boost. Healthcare has actually seen the biggest decrease in Q4 margin expectations (-178 bps, present worth: 7.0%), followed by Products (-119 bps, 8.4%), and Energy (-112 bps, 9.6%). Infotech has actually seen the biggest enhancement in margin expectations (45 bps, 24.5%).

The 2023 and 2024 full-year quotes are presently 11.2% and 11.7% respectively, while the forward four-quarter price quote is now comparable to the 2024 full-year price quote for the next 3 months.

The Splendid 7 has an aggregate Q4 net margin price quote of 21.2%.

Exhibition 6: S&P 500 Net Margin Expectations

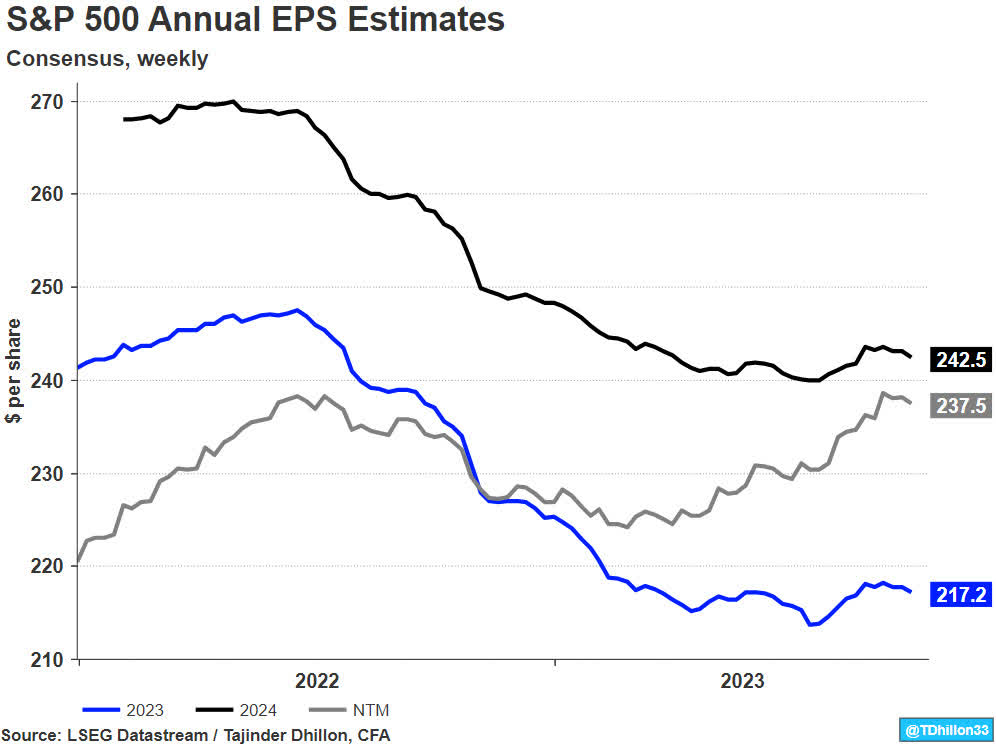

Part 6 – Forward P/E & & PEG Ratio

Utilizing LSEG Datastream, the forward 12-month (F12) EPS is $243.36 per share (Exhibition 7) and sits above the 2024 EPS price quote of $238.76 as the weighting of the computation now takes the 2025 price quote into factor to consider.

Taking a look at the information in a various method, the 2023 and 2024 quotes have actually decreased by 12.3% and 10.6% respectively considering that June 2022. In contrast, the S&P 500 has actually increased by roughly 28% over the exact same duration.

The S&P 500 forward 12-month P/E ratio (time-weighted basis) reveals an existing reading of 19.9 x, which ranks in the 85th percentile (considering that 1985) and an 11.8% premium to its 10-year average (17.8 x). For referral, the trough forward P/E throughout the last 4 economic downturns were as follows: 10.1 x (Oct 1990), 17.3 x (Sept 2001), 8.9 x (Nov 2008), and 13.0 x (March 2020).

Moreover, the S&P 500 ‘PEG’ ratio is presently 1.32 x which ranks in the 65th percentile (considering that 1985) and a 6.4% discount rate to its 10-year average (1.41 x).

Exhibition 7: S&P 500 EPS Price Quotes

Conclusion

Q4 quotes have actually been reduced strongly heading into incomes season which might set a lower bar for corporations to beat expert expectations and surprise to the advantage, as seen in every quarter of 2023 so far.

We continue to keep track of top-line strength and see if Q4 can reveal any enhancement vs. expert expectations, provided the income surprise rate reaching a multi-year low last quarter.

A lot of worrying is the trajectory of price quote modifications keeping an eye out to 2024, as 7 of the 11 sectors have actually seen down modifications to incomes development expectations for Q1, Q2, and Q3 2024.

Editor’s Note: The summary bullets for this short article were picked by Looking for Alpha editors.